Guidance on Filing Form C-S/ Form C-S (Lite)/ Form C

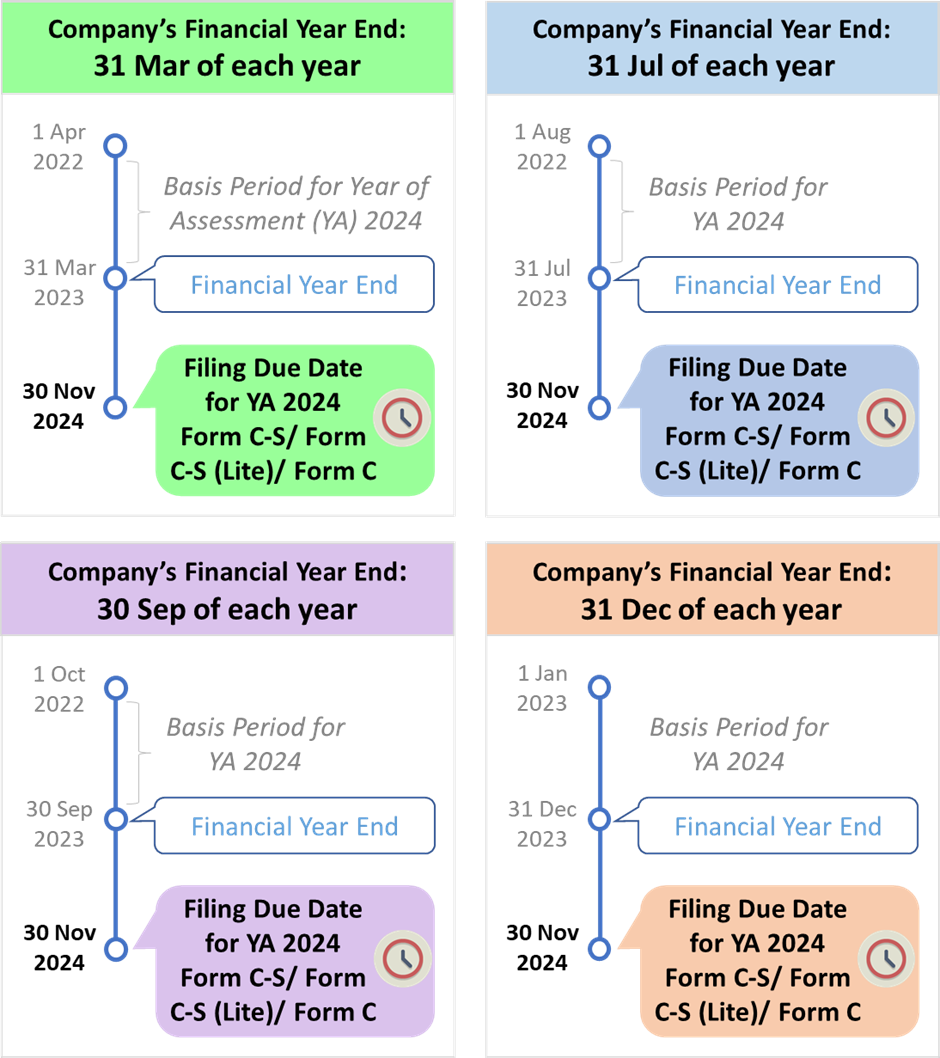

Form C-S/ Form C-S (Lite)/ Form C must be filed by 30 Nov every year to avoid enforcement actions such as composition or summons. The filing due date of 30 Nov provides companies with at least 11 months to file from the time of closing of the accounts.

If your company is new, read Form C-S/ Form C-S (Lite)/ Form C Filing - For New Companies to learn when to file your first Form C-S/ Form C-S (Lite)/ Form C.

Examples Based on Different Financial Year Ends

How to File Form C-S/ Form C-S (Lite)

The File Form C-S/ Form C-S (Lite) digital service for the Year of Assessment (YA) 2024 is available at mytax.iras.gov.sg.

Step 1

Do the following before you start filing:

- Confirm that your company meets the qualifying conditions to file Form C-S. If your company has an annual revenue of $200,000 or below, you can choose to file Form C-S (Lite), a simplified version of Form C-S.

- Ensure that you are duly authorised by your company as an ‘Approver’ for ‘Corporate Tax (Filing and Applications)’ in Corppass. View our step-by-step guides for assistance on Corppass setup.

- Have your Singpass as well as your company’s Unique Entity Number (UEN)/ Entity ID ready.

- Have your company's financial statements, tax computation, and other supporting documents ready.

Step 2

File Form C-S/ Form C-S (Lite) via mytax.iras.gov.sg. Set aside at least 10 minutes to complete Form C-S/ Form C-S (Lite).

For assistance on filing, refer to these step-by-step guides:

- For Companies: User Guide - File Form C-S/ Form C-S (Lite) (PDF, 2MB)

- For Tax Agents: User Guide - File Form C-S/ Form C-S (Lite) (PDF, 2MB)

For more information on filing matters, refer to these guides:

- Explanatory Notes to YA 2024 Form C-S (PDF, 381KB)

- FAQs on filing of Form C-S/ Form C-S (Lite) (PDF, 350KB)

Filing Form C-S/ Form C-S (Lite) for New Companies

If your company's first set of financial statements covers a period of more than 12 months from its date of incorporation, indicate the relevant financial period under Part A of Form C-S/ Form C-S (Lite).

When completing Part B, you need to:

- Attribute the company's adjusted profit/ losses before other deductions to 2 YAs*. This is because the basis period for each YA should not exceed 12 months.

- Complete the line items for 2 YAs in Form C-S/ Form C-S (Lite).

* Time apportionment basis may be used if you are unable to directly identify the adjusted profit/ losses before other deductions to the corresponding basis period for each YA.

How to File Form C

The File Form C digital service for the Year of Assessment (YA) 2024 is available at mytax.iras.gov.sg.

Step 1

Do the following before you start filing:

- Ensure that you are duly authorised by your company as an ‘Approver’ for ‘Corporate Tax (Filing and Applications)’ in Corppass. View our step-by-step guides for assistance on Corppass setup.

- Have your Singpass as well as your company’s Unique Entity Number (UEN)/ Entity ID ready.

- Have your company’s financial statements, detailed profit and loss statement, tax computation and other supporting documents ready in softcopy for submission to IRAS.

- Ensure that softcopy documents are in pdf format. You can convert them to pdf format with a software converter (e.g. PrimoPDF).

- Ensure that hardcopy documents are scanned into pdf files and the images are clear.

- Use font size of at least 11 for your attachments.

- Choose resolution of ‘100dpi black and white’ if you need to reduce the file size of attachments.

Step 2

File Form C via mytax.iras.gov.sg and attach the company’s financial statements, detailed profit and loss statement, tax computation and other supporting documents. Set aside at least 30 minutes to complete Form C.

For assistance on filing, refer to these step-by-step guides:

- For Companies: User Guide - File Form C (PDF, 2.4MB)

- For Tax Agents: User Guide - File Form C (PDF, 2.3MB)

For more information on filing matters, refer to these guides:

- Explanatory Notes to YA 2024 Form C (PDF, 370KB)

- FAQs on filing of Form C (PDF, 343KB)

Filing Form C for New Companies

If your company's first set of financial statements covers a period of more than 12 months from its date of incorporation, indicate the relevant financial period under the ‘General Info’ section of Form C.

In the subsequent pages, you need to:

- Attribute the company’s trade/ business income/ loss to 2 YAs*. This is because the basis period for each YA should not exceed 12 months.

- Complete the line items for 2 YAs in Form C.

* Time apportionment basis may be used if you are unable to directly identify the trade/ business income/ loss to the corresponding basis period for each YA.

Points to Note When Filing

Online Help

.jpg?sfvrsn=5a271827_3)

Click on the iHelp icon <> if you require on-the-spot guidance as you file Form C-S/ Form C-S (Lite)/ Form C.

Pre-filled Information

The following amounts are pre-filled in Form C-S/ Form C-S (Lite)/ Form C, where available:

- Unutilised Capital Allowances brought forward

- Unutilised Losses brought forward

- Unutilised Donations brought forward

- Current year Approved Donations

- Unutilised Investment Allowances brought forward (for Form C)

The pre-filled information is based on the carried forward amounts in the last assessment raised by IRAS for the immediate preceding YA. This applies even if the assessment for the immediate preceding YA is under objection or query.

If the return for the immediate preceding YA is under review, the pre-filled information will be based on the carried forward amounts declared in the Form C-S/ Form C-S (Lite)/ Form C of the immediate preceding YA.

The amounts are pre-filled for your easy reference and you should verify the accuracy of the information. If there is any discrepancy in the details (i.e. the company’s carried forward amounts in its records differ from the pre-filled records), you may update the pre-filled amounts in the relevant boxes under ‘Company's Declaration’ (with the exception of current year donations).

The 250% deduction for donations is granted based on information obtained from the Institutions of a Public Character (IPCs). Upward adjustments are not allowed unless your company adopts a non-Singapore Dollar functional currency. View the details of the current year approved donation amounts in the View Donations digital service at mytax.iras.gov.sg.

If your company has made an approved donation that is not reflected in the View Donations digital service, it may be due to:

- Differences in receipting date

The IPC may have recorded your donation in a later financial period and a deduction will be accorded in the corresponding YA.

- Failure to provide your company’s Unique Entity Number (UEN) to the IPC

Update your donation record with the IPC and IRAS will amend your assessment when we receive the updated record.

If your company has adopted a non-Singapore Dollar functional currency for the financial period, ensure that the ‘Functional Currency’ in the Corporate Profile Page is updated accordingly. You will then be allowed to key in the Singapore dollar equivalent amount of your current year donation in the ‘Company’s Declaration’ box.

Save Draft Function

If you are unable to complete your filing in 1 session, save the Form C-S/ Form C-S (Lite)/ Form C as 'draft'. The draft will be retained in the portal up to the filing due date. You can access the draft anytime till the filing due date and make the necessary amendments before you file your Form C-S/ Form C-S (Lite)/ Form C.

If you or your tax agent needs to present the completed Form C-S/ Form C-S (Lite)/ Form C to relevant personnel/ clients before filing with IRAS, you may use the ‘Save Draft’ function and print out the completed Form C-S/ Form C-S (Lite)/ Form C at the ‘Confirmation Page’.

Timeout

If you are inactive on the Form C-S/ Form C-S (Lite)/ Form C filing service for more than 15 minutes, the system will prompt you to respond within 2 minutes. If there is no activity within the 2 minutes, you will be automatically logged out of mytax.iras.gov.sg.

Acknowledgement of Successful Filing

You will receive an instant acknowledgement of receipt upon successful filing of Form C-S/ Form C-S (Lite)/ Form C. The same acknowledgement page will be available at mytax.iras.gov.sg under the View Notices/ Letters - Corporate Tax digital service. Please do not submit the acknowledgement page to IRAS.

FAQs

- My company was dormant and had previously been granted a waiver to file Form C-S/ Form C-S (Lite)/ Form C. How can I request for the Form C-S/ Form C-S (Lite)/ Form C now that my company has recommenced business/ received income? Notify IRAS within 1 month from the date of commencement of your business or earning/ receiving the income by emailing us via myTax Mail to request for the Form C-S/ Form C-S (Lite)/ Form C, with all of the following details (indicate ‘N/A’ if not applicable):

- Subject header: ‘Recommencement of business and request for Corporate Income Tax Return’

- Name and Unique Entity Number (UEN) of the company

- Date of recommencement of business in dd/mm/yyyy format

- Date of receipt of other source(s) of income (e.g. interest, dividend, rent) in dd/mm/yyyy format

- New principal activity and the effective date of change in dd/mm/yyyy format together with a copy of BizFile+ extracted from the Accounting and Corporate Regulatory Authority (ACRA) showing the principal activity of the company

Documents to Prepare

Your company is required to prepare its financial statements, tax computation and other supporting documents before completing Form C-S/ Form C-S (Lite)/ Form C.

For Filing Form C-S/ Form C-S (Lite)

Companies filing Form C-S/ Form C-S (Lite) must prepare:

- Audited/ unaudited financial statements

- Tax computation and supporting schedules

- Declaration for the Purpose of Claiming Writing-Down Allowances for Intellectual Property Rights (IPRs) under Section 19B of the Income Tax Act 1947 (PDF, 93KB) (if applicable)

- Other supporting documents

These documents should be retained and submitted upon IRAS’ request, except for the declaration form for claiming writing-down allowances, which is to be filed together with Form C-S/ Form C-S (Lite).

Audited/ Unaudited Financial Statements

Dormant companies and companies that qualify as a ‘small company’ are not required to have their financial statements audited, as provided for under the Companies Act 1967.

For Filing Form C

Companies filing Form C must prepare:

- Audited/ unaudited financial statements

- Tax computation and supporting schedules

- Form IRIN 301 (Additional Information on Income and Deduction)

- Detailed Profit and Loss Statement 1

- Relevant claim forms such as Group Relief Forms (Form GR-A (PDF, 619KB) and Form GR-B (PDF, 639KB)), Research & Development Claim Form (YA 2018 and before) (PDF, 377KB), and Research & Development Claim Form (YA 2019 and onwards) (PDF, 1MB)

- Revised tax computation(s) for prior Years of Assessment (YAs) 2 (only applicable if the company is claiming Loss Carry-Back Relief and/or reporting income that was not reported in prior years)

- Declaration for the Purpose of Claiming Writing-Down Allowances for Intellectual Property Rights (IPRs) under Section 19B of the Income Tax Act 1947 (PDF, 93KB) (if applicable)

- Other supporting documents

These documents must be filed together with Form C, unless it is specifically mentioned that they should be retained and submitted only upon IRAS’ request.

1 This can be filed together with either the audited/ unaudited financial statements or tax computation and supporting schedules.

2 Companies that need to file revised tax computations after filing their Form C due to errors should file the revised tax computations via the Revise/ Object to Assessment digital service. Such revised tax computations should not be filed together with Form C under the Submit Document digital service.

Other Documents

These documents listed below should be prepared at the time of filing of the Corporate Income Tax Return. They should be retained by the company and submitted upon IRAS’ request. This list is not exhaustive.

Costs of Registering Intellectual Property Rights

- Brief description of the intellectual property

- Country/ territory in which the intellectual property was registered

- Name and tax reference number of joint-owners (if any)

- Breakdown of registration costs

- Confirmation that the intellectual property is/ will be legally owned by the company

- Confirmation that the economic benefits from the exploitation of the intellectual property is/ will be accrued to the company

Deduction Claimed under Section 14N for Expenditure on Renovation or Refurbishment Works

- An itemised list of the renovation or refurbishment works done to the business premises, including the related costs incurred, with addresses of the premises

- Confirmation on the itemised list that the renovation or refurbishment works do not require the approval of the Commissioner of Building Control

- Invoices and payment details of the relevant expenditures

For R&D activities outsourced directly by your company to an overseas R&D organisation:

- Name and description of the intellectual properties arising from the outsourced R&D that are owned/ to be owned by the company in Singapore

- Brief description of the overseas R&D organisation, including the organisation's address

For R&D activities undertaken under a cost-sharing agreement:

- Name and description of the intellectual properties arising from the R&D under the cost sharing agreement

- Copy of the cost-sharing agreement

Your company must maintain proper documentation of its R&D projects to substantiate its R&D claims to IRAS when requested. All documentation should be maintained from the start of the R&D project, rather than as an after-event. Examples include test results, award of a patent resulting from R&D and press statements. View more examples of information/ documentation that help to substantiate R&D claims (PDF, 1.21MB).

Directors' Fees & Remuneration

Where your company claims a tax deduction for directors' fees:

- Date that the director's fees were approved

- Amount approved

- Year in which any unapproved amount is written back (if applicable)

- Amount (if any) of director's fees approved in arrears at the relevant Annual General Meeting (AGM) but the directors were entitled to the fees only after the accounting year in which such fees were approved

Double Tax Deduction for Internationalisation Scheme (Sections 14B/14H)

- Date of approval letter from Enterprise Singapore or Singapore Tourism Board, if applicable

- Details of event

- Period of event

- Claim amount per certificate, if applicable

- Details of eligible expenses incurred

- Amount qualifying for further deductions

Exchange Gain/ Loss

- Itemised breakdown of the underlying capital or revenue transactions/ assets/ liabilities that gave rise to the foreign exchange differences.

Please refer to our e-Tax Guide on "Income Tax Treatment of Foreign Exchange Gains or Losses for Businesses (PDF, 352.3KB)" for a sample breakdown format.

Foreign Income Exempted from Tax as a Result of Incentive Granted by Foreign Jurisdiction (‘Subject to tax’ Concession)

- Declaration that the foreign jurisdiction has exempted the specified foreign income from tax because of substantive business activities carried on by your company in that foreign jurisdiction

- Copy of the tax incentive certificate/ approval letter issued by the foreign jurisdiction. In the case of a foreign-sourced dividend, a dividend voucher (if available) stating that the dividend is exempt from tax due to a tax incentive granted to the payer company for carrying on substantive business activities in that foreign jurisdiction

Gains from Disposal of Ordinary Shares in Another Company (Section 13W)

- Whether your company, the divesting company, is in the insurance business

- Name of the investee company

- Whether the investee company is in the business of trading Singapore immovable properties or principally carries on the activity of holding Singapore immovable properties (other than the business of property development). For non-listed shares disposed on or after 1 Jun 2022, whether the investee company:

- Is in the business of trading immovable properties (situated in Singapore or elsewhere)

- Principally carries on the activity of holding immovable properties (situated in Singapore or elsewhere)

- Has undertaken property development activities in Singapore or elsewhere. If so: (i) how the immovable properties developed are used by the investee company; and (ii) whether there have been property development activities carried out in the past 60 months prior to the disposal of shares by the divesting company

Gain/ Loss on Sale of Property

- Address of the property

- Date of purchase and purchase price

- Date of sale and sale price

- Name and address of the purchaser

- Whether the purchaser is related to the company, its directors or its shareholders, and the nature of the relationship, if applicable

Gain/ Loss on Sale of Shares (excludes gains exempted under Section 13W)

For each block of shares disposed:

- Name of the company

- Date of purchase and purchase price

- Date of sale and sale price

- Number of shares purchased and sold

- Reason(s) for the purchase and sale

- Basis of arriving at the gain/ loss on disposal

- Reason(s) for treating the gain as not taxable or loss as deductible, if applicable

Impairment Loss in respect of Bad Debts/ Provision for or Doubtful Debt

- Details of debts (name and amount owed by each debtor) that were not incurred in respect of the trade or business, such as loans and advances

- Details of debts that were taken over in the case of a transfer or merger of business

- Details of debts in respect of a trade that had ceased, including any activity granted with pioneer incentive that had ceased

- Segregation of debts relating to the different tax rate categories

Where the amount of impairment loss exceeds $250,000 for trade debts owed by related parties, additional information is required:

- Relationship between the company and the trade debtor

- Whether normal credit policy and terms were extended to the related party. If not, provide the reasons for the extended credit policy and terms

- Reasons the related party was unable to repay the trade debt

- Whether steps were taken to recover and enforce the debts. If not, provide the reasons for not enforcing the debts

Land Intensification Allowance (LIA)

- Copy of the letter of offer from the Singapore Economic Development Board (EDB) or Building and Construction Authority (BCA)

- Details of qualifying capital expenditure incurred on the construction, renovation or extension of the approved LIA building or structure and the computation of the Initial Allowance and Annual Allowance to be claimed (refer to Annex B of EDB's LIA Brochure and Annex A of BCA’s LIA Brochure for a worked example)

- Copy of the verification form submitted to EDB or BCA previously for the construction, renovation or extension completed during the Year of Assessment (YA)

- Approval letter from EDB or BCA that allows the company to continue claiming LIA for the basis period where there are any changes to qualifying user(s) and/ or use(s) that count towards the minimum 80% gross floor area (GFA) requirement

Mergers & Acquisitions Allowance (M&A) (Section 37O)

- Confirmation by a responsible officer of the acquiring company that all qualifying conditions for M&A allowance have been met

- Copy of the executed share purchase agreement, or if such an agreement is not available, the instrument of transfer

- Copy of the latest statement of financial statements of the target company that is within 24 months from the date of agreement or transfer. This is regardless of whether the target company is incorporated in Singapore or outside Singapore

- Independent professional valuation report* of the ordinary shares of the target company acquired under any of the following circumstances:

- Target company is incorporated outside Singapore

- Acquisition is funded by way of the acquiring company's issuance of shares/ units and the market value of such shares/ units is not readily available

- Acquiring company does not wish to determine the M&A allowance based on the Net Asset Value (NAV) of its shares/ units

* The requirement for an independent professional valuation report is waived when:

- The acquiring company and the shareholders in the target company are not related to each other on the date of share acquisition; and

- The value of the share acquisition is $5 million or below.

Motor Vehicle Expenses

- Registration number of and amount applicable to each vehicle

- Amount applicable to private cars and Q-plated and RU-plated cars registered on or after 1 Apr 1998

1 Year Write-off for New Diesel-Driven Goods Vehicles & Buses

- Vehicle registration books or cards of the existing and new vehicles

- Certificate of Entitlement (COE) of the existing vehicle

- Approved De-registration Application Form for the de-registration of the existing vehicle

Purchase of Property

- Address of the property

- Date of purchase and purchase price

- Name and address of the vendor

- Whether the vendor is related to the company, its directors or its shareholders, and the nature of the relationship, if applicable

- Purpose of acquisition (e.g. for rental, resale)

- Use of the property since its acquisition and duration of each use. If the property was vacant at any point in time, specify the period

- Means of financing the purchase

Purchase of Shares

For each block of shares purchased:

- Name of the company

- Date of purchase and purchase price

- Number of shares purchased

- Reason(s) for the purchase

- Means of financing the purchase

Rental Income

- Statement of gross rental and direct expenses incurred on each property and the rental period

Securities Lending & Repurchase Arrangements

- Distributions passed on

- Compensatory payments made

- Economic ownership remains with the transferor

Tax Set-Offs (Double Taxation Relief (DTR) & Unilateral Tax Credit (UTC))

- Jurisdiction in which foreign tax was paid

- Nature of the income

- Description of the services rendered, and whether the income was derived through a permanent establishment in the foreign jurisdiction and your basis for this claim, if applicable

- Name of the payer

- Date of withholding tax receipt/ voucher

- Gross amount of income, withholding tax rate and amount of tax withheld in foreign currency as well as the corresponding S$ amount

- For a claim of DTR, the relevant Article of the Avoidance of Double Taxation Agreement under which the tax was withheld

- Withholding tax receipt/ voucher*

* If this is not available, a letter (XLSX, 12KB) certifying that foreign tax has been/ will be paid** on the income remitted may be submitted instead. The certification must be made by either a director/ auditor of the company, a public accountant in Singapore or a public accountant in the country/ territory where the income was derived.

** IRAS may subsequently require the company to confirm the amount of foreign tax paid after it has been paid.

Learn more about DTR and UTC.

Checking the Status of Filing

You can check the status of your company’s tax assessment via mytax.iras.gov.sg or IRAS Bot. These services are available 24 hours daily.

Via Digital Services

- Log in to mytax.iras.gov.sg.

- Select the View Corporate Tax Filing Status digital service to check the status of your company’s tax assessment.

For assistance on checking the filing status, refer to these guides:

- For Companies: User Guide - View Corporate Tax Filing Status (PDF, 515KB)

- For Tax Agents: User Guide - View Corporate Tax Filing Status (PDF, 582KB)

- FAQs on viewing corporate tax filing status (PDF, 218KB)

Via IRAS Bot

Our IRAS Bot can assist companies with the following status checks for Corporate Income Tax:

Form C-S/ Form C-S (Lite)/ Form C (for the current and 3 previous Years of Assessment):

- Tax Assessment Status

- Filing Status

Corporate Income Tax Payment:

For our IRAS Bot to assist with your status check, please have the company’s tax reference number* ready.

* The company's tax reference number is its Unique Entity Number (UEN), which falls within the categories below:

| Local Companies with UEN | E.g. 200312345A |

| Foreign Companies with UEN | E.g. T08FC1234A

|

Revising Form C-S/ Form C-S (Lite)/ Form C After Filing

You should complete Form C-S/ Form C-S (Lite)/ Form C carefully to avoid making mistakes. However, if errors are discovered after filing Form C-S/ Form C-S (Lite)/ Form C, you may revise the amount declared.

How to File Revisions to Form C-S/ Form C-S (Lite)/ Form C

Go to the Revise/ Object to Assessment digital service at mytax.iras.gov.sg to submit your revised tax computation(s).

For assistance on revising your Form C-S/ Form C-S (Lite)/ Form C, refer to these guides:

- For Companies: User Guide - Revise/ Object to Assessment (PDF, 3.3MB)

- For Tax Agents: User Guide – Revise/ Object to Assessment (PDF, 3.4MB)

- FAQs on revising or objecting to assessment (PDF, 258KB)

1. For revisions to Form C-S/ Form C-S (Lite), attach the company’s financial statements as well.

2. Disclosure of errors or omissions via revised income tax computation(s) (excluding situations where companies are selected for an audit/ investigation by IRAS) may be considered a Voluntary Disclosure.